NATIONAL carrier Singapore Airlines (SIA) on Friday (Nov 8) reported a net profit of S$290 million for the second quarter ended Sep 30, sliding 59 per cent from S$707 million in the corresponding period in the previous year.

This is despite revenue for the period rising 2 per cent to S$4.8 billion, from S$4.7 billion a year ago.

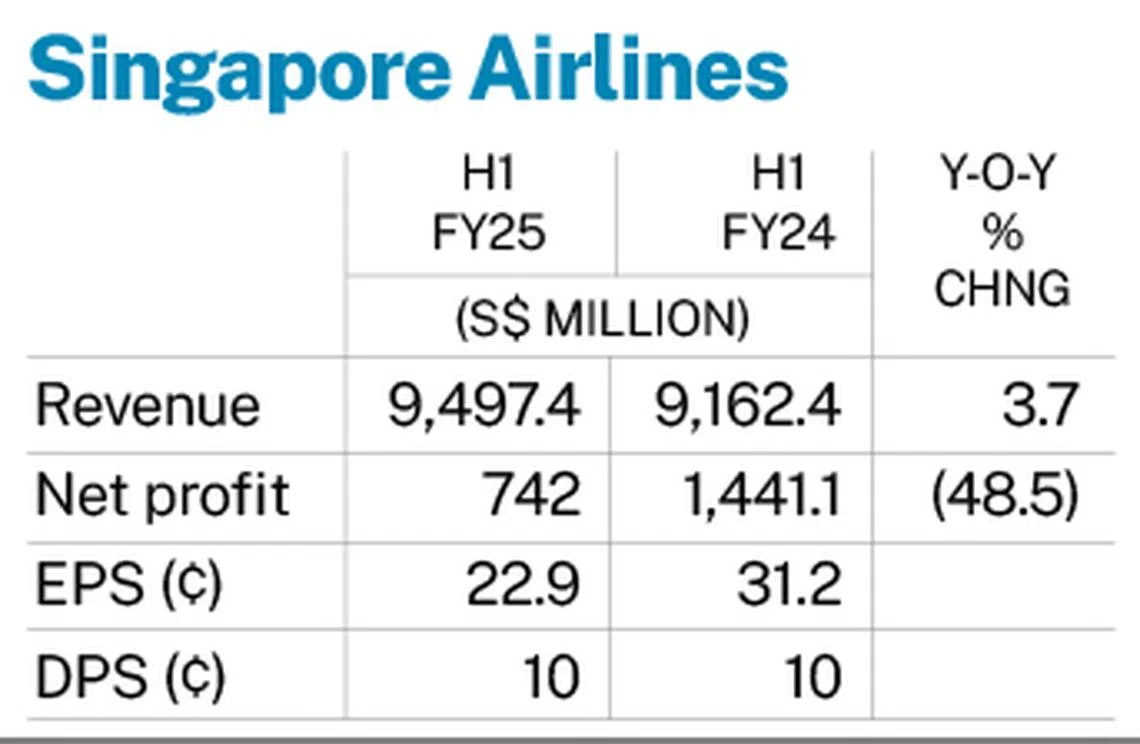

The lower profit was mainly due to weaker operating performance, lower net interest income, and loss on disposal of aircraft, spares, and spare engines versus a gain last year. However, it was partially offset by a higher share of associated companies’ profits and lower tax expense.

The group has declared an interim dividend of S$0.10 per share, payable on Dec 11.

On a half-yearly basis, net profit came in at S$742 million, declining 48.5 per cent from S$1.4 billion in the same period a year ago. This translates to a first-half earnings per share of S$0.229, compared with S$0.312 in the previous corresponding period.

Revenue for H1 was S$9.5 billion, up 3.7 per cent from S$9.2 billion a year ago.

BT in your inbox

Start and end each day with the latest news stories and analyses delivered straight to your inbox.

The group noted that demand for air travel remained healthy in the first six months of FY2025, with Singapore Airlines and its budget arm Scoot carrying 19.2 million passengers, a 10.8 per cent year-on-year increase.

However, passenger traffic growth of 7.9 per cent trailed the SIA Group’s passenger capacity expansion of 11 per cent, resulting in a 2.4 percentage point decline in group passenger load factor to 86.4 per cent.

The passenger load factor measures how much the airline’s passenger capacity has been utilised. It is calculated by dividing the airline’s revenue passenger kilometres by its available seat kilometres.

SIA and Scoot achieved passenger load factors of 85.7 per cent and 88.6 per cent, respectively.

Air freight, meanwhile, was bolstered by strong e-commerce flows and ongoing disruptions to sea freight. The cargo load factor increased by 4.7 percentage points to 57.4 per cent, as the 20 per cent rise in loads outpaced the 10.2 per cent increase in capacity. This reflected the strong demand in this sector.

Increased competition and higher passenger capacity in key markets exerted pressure on passenger yields, which fell 5.6 per cent. On the cargo front, the yield was 13.4 per cent lower amid the continued recovery in bellyhold capacity.

As yields moderated, the group’s operating profit came in at S$795.6 million in the first half of FY2025, down 48.8 per cent from S$1.6 billion a year ago.

In terms of fleet development, SIA added four Boeing 787-10 aircraft in the second quarter.

As at Sep 30, 2024, the group’s operating fleet consisted of 205 aircraft with an average age of seven years and five months. This comprises SIA’s 146 passenger aircraft and seven freighters, and Scoot’s 52 passenger aircraft. The group has 84 aircraft on order.

SIA recently announced that it is investing S$1.1 billion to install new long-haul cabin products in 41 Airbus A350-900 aircraft. The first retrofitted plane will enter service in the second quarter of 2026, and SIA aims to complete the programme by end-2030.

The group expects demand for air travel to be robust in the second half of the financial year, but added that the operating landscape “will continue to be competitive”.

“Heading into the year-end peak, air freight demand is expected to stay healthy,” said SIA.

Shares of SIA ended on Friday at S$6.45, down S$0.04 or 0.6 per cent, before the announcement.